“Buyers with good credit scores will pay even more to cover for those with bad credit."

A sale pending sign hangs in front of a property in San Francisco, April 18, 2023. (AP)

On May 1, the U.S. government updated its mortgage fee system. Some, but not all, homebuyers with higher credit scores could see increased fees for a new mortgage, and people with lower credit scores will generally see fees decrease. But most high-credit homebuyers are not subsidizing fee reductions for low-credit homebuyers.

Even with the changes, people with lower credit scores still typically pay higher fees overall than people with better scores.

There is no evidence that President Joe Biden was involved in implementing the update, and the White House said Biden’s administration did not direct the action.

As anger and confusion mounted over changes to the U.S. government’s mortgage fee system, Republican presidential candidate Nikki Haley waded into the fray.

"Thanks to Joe Biden, starting May 1, your mortgage costs may go up," Haley tweeted April 21. "Buyers with good credit scores will pay even more to cover for those with bad credit. Punishing those who act responsibly: it's the Biden way."

But most high credit-score homebuyers are not subsidizing fee reductions for low credit-score homebuyers, government agencies and experts said.

"Higher-credit-score borrowers are not being charged more so that lower-credit-score borrowers can pay less," Federal Housing Finance Agency Director Sandra L. Thompson said April 25. "The updated fees, as was true of the prior fees, generally increase as credit scores decrease for any given level of down payment."

The changes, Thompson said, don’t represent "pure decreases for high-risk borrowers or pure increases for low-risk borrowers." Many people with high credit scores or large down payments will see their fees decrease or remain flat, she said.

Some people with good credit scores could see fees for a new mortgage increase, but that won’t be true for everyone. Although people with lower credit scores generally will see fees decrease, they still typically pay higher fees overall than high credit-score buyers.

The Federal Housing Finance Agency, which oversees Fannie Mae and Freddie Mac, the country’s largest home loan guarantors, announced the changes in January, partly to help support borrowers with limited income or wealth.

We found no evidence that Biden was involved in the adjustment.

"The administration did not direct this action," White House spokesperson Robyn Patterson wrote in an email.

PolitiFact asked Haley’s campaign for comment but received no response.

The update stems from changes to loan level price adjustments, known as LLPAs. These fees, levied by Fannie Mae and Freddie Mac, are based on how much credit risk buyers pose. The fees vary by borrower and are based on various loan features, such as the person’s credit score rating and their down payment amount, as well as other factors.

The pricing structure was introduced during the 2008 economic recession after Fannie and Freddie were taken into government conservatorship because they were underfunded and overexposed to risk. The structure has been adjusted several times since.

The loan level price adjustments are not interest rates, experts noted. They are upfront fees paid over a loan’s duration that equate to small monthly amounts and apply only to conventional loans. They don’t affect mortgages insured or guaranteed by other agencies, including the Federal Housing Administration.

The latest update to the pricing structure was announced Jan. 19. It’s one of several changes the Federal Housing Finance Agency has introduced — including an elimination of the fees for some first-time homebuyers — since it launched a review in 2021.

Under the new rules:

A buyer with a 640 credit score — which is considered fair or below average — who makes a 20% downpayment on a home purchase must pay a 2.25% fee.

A buyer with a 740 credit score — considered very good — who also puts down around 20% must pay a 0.88% fee.

That’s a difference of about 1.375%, or just over $4,000 on a $300,000 mortgage.

This still represents a reduction for the homebuyer with the 640 credit score — who would have paid a 3% fee under the previous framework — and an increase for the homebuyer with the 740, who previously had a 0.5% fee. But buyers with lower scores are still paying more in the end.

"The interpretation of what is happening is flat out wrong," said Janneke Ratcliffe, vice president of the Urban Institute’s housing finance policy center.

"What they have done in this change is just basically move some dials around on the numbers," Janneke said. "What people are getting wrong is this interpretation that lower-risk borrowers are paying more than higher-risk borrowers, which is not so, she said, adding that across the board, "the lower the risk, the less you pay."

Homebuyers with credit scores above 780, meanwhile, will see fees reduced or remain the same as the new framework breaks down credit scores into more categories.

Before, someone with a 782 credit score was in the same category as someone with a 742 credit score and paid the same fee. Now that they are in different categories, the homebuyer with a 742 might pay a little more, while the homebuyer with the 782 might pay a little less.

In an April 29 appearance on CNN’s "This Morning Weekend," Bob Broeksmit, CEO of the Mortgage Bankers Association, a nonprofit representing the real estate finance industry, said the mortgage fee adjustment corrects these anomalies that appeared in the previous pricing.

"Under the old grid, there were times that, if your credit score went from 680 to 679 — a 1 point difference that I think most people would say is not consequential — you could pay a point and a quarter more than if you had a 680, and that just made no sense," Broeksmit said.

The Federal Housing Finance Agency has also raised fees on second-home loans, high-balance loans and cash-out refinances. These are higher fees imposed on properties such as vacation homes, investor properties and million-dollar homes.

Housing finance policy experts said these fee increases for the wealthy matter, because the deals they govern generate most of the revenue. The experts added that the fee increase enabled the government to decrease costs for buyers with limited wealth or income. The higher fees are imposed on a small subset of all buyers.

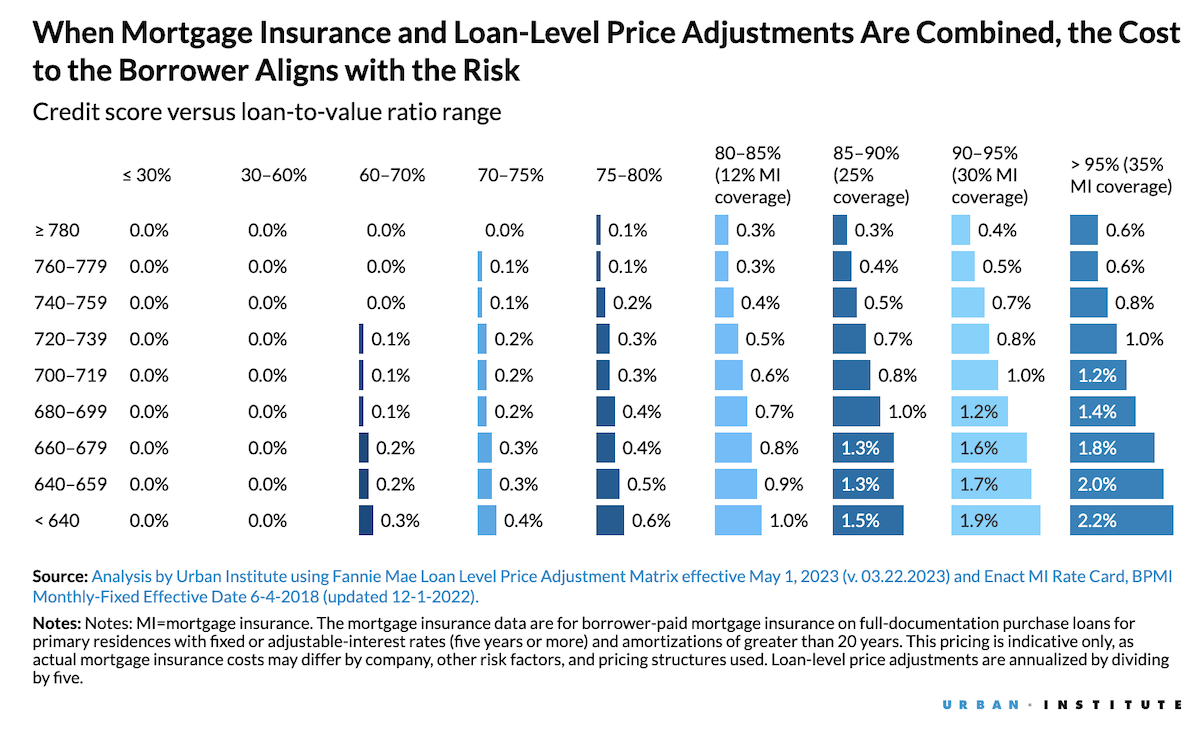

Critics have said the new framework charges some homebuyers less in fees if they make a smaller down payment and argued that this shows the Federal Housing Finance Agency is using discounts for some to pay for increases on others. But experts say this reasoning ignores the role of mortgage insurance, which buyers must purchase if they put down less than 20%.

People in those smaller-down payment, lower-credit score categories must pay more for this insurance for a longer period. This shifts some of the risk away from Fannie Mae and Freddie Mac to the insurer, allowing the government to charge a lower fee. But people in this situation still typically pay more overall when buying a home.

The Urban Institute broke this down in an April 27 report, noting that after adding in the cost of the mortgage insurance fee to someone’s total cost for a mortgage, "the apparent disconnection between risk and price" that appears in some of these new charts "disappear, with borrowers’ payments rising or falling according to the risk they pose."

Haley said, "Buyers with good credit scores will pay even more to cover for those with bad credit."

That misrepresents the fee adjustment. Homebuyers with higher credit scores aren’t subsidizing fee reductions for lower-credit homebuyers.

The Federal Housing Finance Agency called the claim inaccurate, and said most of the revenue generated to offset reductions for low-credit buyers comes from higher fees on million-dollar homes and investor properties, not from raising prices on people with better credit. This group is a small subset of all buyers.

The statement contains an element of truth because some homebuyers with good credit scores will pay more under the changes. But it ignores that most homebuyers aren’t subsidizing fee reductions for other homebuyers and that people with low credit pay more in fees overall.

We rate it Mostly False.

Nikki Haley, Twitter post, April 21, 2023

Facebook post, April 22, 2023

Facebook post, April 21, 2023

Federal Housing Finance Agency, FHFA Announces Updates to the Enterprises’ Single-Family Pricing Framework, Jan. 19, 2023

Federal Housing Finance Agency, Setting the Record Straight on Mortgage Pricing: A Statement from FHFA Director Sandra L. Thompson, April 25, 2023

Fannie Mae Loan-Level Price Adjustment Matrix, Updated March 22, 2023

Urban Institute, No, Fannie Mae and Freddie Mac Aren’t Penalizing People with Good Credit to Help People with Bad Credit, April 25, 2023

Urban Institute, Fannie Mae and Freddie Mac’s New Pricing Is Not Punishing Those with Better Credit: Follow the Numbers, April 27, 2023

Mortgage News Daily, Is There Really a New, Unfair Mortgage Tax on Those With High Credit?, April 21, 2023

The Mortgage Reports, Loan-Level Pricing Adjustments (LLPA): A Complete Guide For Mortgage Borrowers, April 26, 2023

Snapstream, CNN "This Morning Weekend" clip, April 29, 2023

Phone interview, Janneke Ratcliffe, vice president of the housing finance policy center at the Urban Institute, April 27, 2023

Email/Phone interview, Federal Housing Finance Agency media office, April 26-27, 2023

Email interview, Robyn Patterson, spokesperson at the White House, May 1, 2023

In a world of wild talk and fake news, help us stand up for the facts.